Three ways the latest inflation figures affect you

Getty Images

Getty ImagesIt's becoming clearer how a war thousands of miles away is hitting pockets here in the UK, with the latest figures showing inflation has risen to 3.3% largely due to higher fuel prices.

With warnings of higher food costs and travel fares also looming, how high could inflation get? And what could it mean for borrowers and savers around the country?

Here are three things you need to know.

1. It's not only up from here

It may feel like the only way for is up for the rate of prices rises, otherwise known as inflation. But that's not necessarily true, especially in the short run.

The domestic energy price cap fell this month, as that is fixed several months behind the moves in global energy markets, so the cap reflects what was happening some time ago.

That means the average energy bill for a household using a typical amount of gas and electricity will be about £10 a month lower from this month, which will put some downward pressure on inflation.

However, it's worth noting that energy bills are expected to rise again with the next price cap from July, thanks largely to the war.

Then there are fuel prices themselves. Petrol prices have started to inch down in recent days, as the wholesale oil price has calmed, although they remain about 25p above what they were before the war per litre and diesel remains more than 40p higher.

And then there's the jump in airfares in March's figures. They actually reflect the relatively early timing of Easter.

This year, the return leg of the long-haul flights they monitor had a return date of the Tuesday after Easter Sunday, at the height of peak season. And, as we tend to book in advance, the ONS collected the info on fares in February, so there was no impact from the war.

When that happens, the inflation figures tend to record airfares easing the following month.

Those factors have led analysts to think inflation could potentially dip below 3% in April.

After that, analysts think inflation could peak near 4% this year, a fraction of the 11% we saw in 2022 at the start of the war in Ukraine.

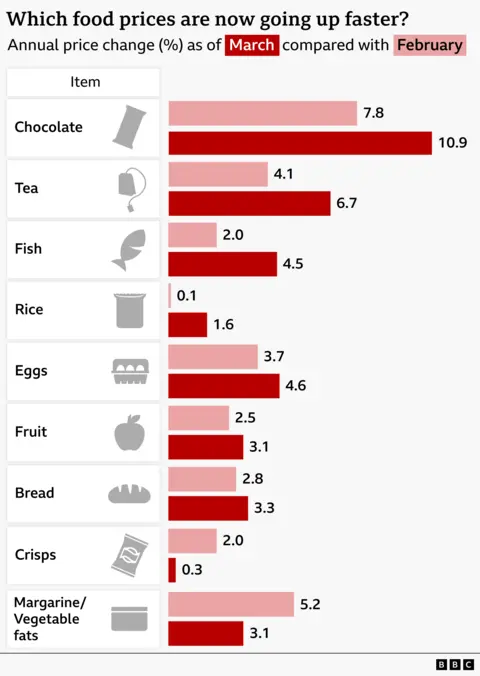

2. Food prices could have a way to go

There appears to have been a seasonal bump behind the rise in food inflation, given it was concentrated in Easter-related items such as confectionery and meat.

Despite that, you shouldn't get too relaxed as other price pressures will emerge, just much more gradually.

In the case of food, producers tend to buy the items most affected by this war such as energy and fertiliser months in advance, so it can be up to a year or more until we notice changes in prices in the supermarket aisles.

The food industry and supermarkets are energy-intensive industries, which means they face risks from higher energy costs.

While the Food and Drink Federation is warning that their members could be increasing prices by 9 or 10% by the end of the year, that might not come to pass.

Customers are more stretched than they were in 2022, more cautious after years of climbing prices. They are also wary of spending as the jobs markets remains challenging.

Many have already traded down to more affordable options as far as they can in spending habits, so retailers may find it harder to pass on higher costs on as price rises, without damaging custom.

And the prices of foodstuffs such as wheat have not rocketed as they did in 2022 as there isn't the risk to supplies. Ukraine is a key source of stables including wheat and sunflower seeds.

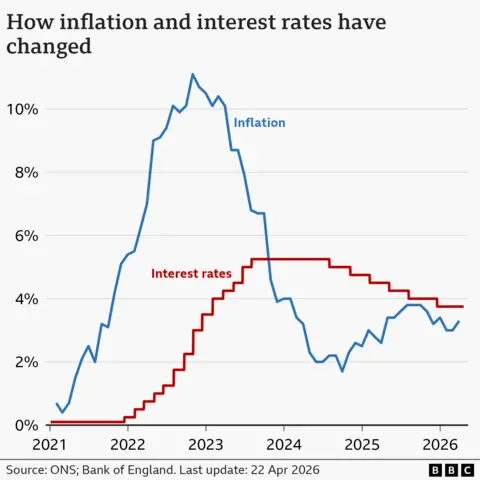

3. Where does that leave interest rates?

The Bank of England's job is to get inflation down to its 2% target and keep it there. Ahead of the war, with inflation set to dwindle, rate cuts seemed to be on the cards.

But, as we know, a lot has changed. The outlook for inflation, especially in the early weeks of the war, had some predicting rates would rise, perhaps several times.

The Bank has suggested it would take a more cautious and pragmatic approach. It knows higher rates can't influence global energy prices. And an energy price shock can knock the winds out of spending and so growth; rate rises could just make that worse.

So, particularly as oil and gas prices have calmed recently, economists are increasingly thinking that the Bank will try to gauge how fleeting the impact on inflation is likely to be before deciding whether or not to raise rates. That means a change at its meeting next week looks unlikely.

As these expectations of rate rises have eased a bit, the rates for fixed rate mortgages have also started to ease, after climbing rapidly over the last month or so.

And that cost of borrowing is ultimately of course, a cost-of-living pressure for not just homeowners but also landlords and their tenants.

However, no interest rate rises this year would mean no change to rates for savers.

There is, of course, much that remains uncertain as this war continues, but there is one silver lining: for most households, incomes have been rising faster than prices in recent times.

It may not feel like it, but the squeeze for many has eased. Although there too, the outlook is not entirely clear.